Quick Answer

To get pre-approved for a mortgage, submit an application with proof of income (pay stubs or tax returns), bank statements, asset documentation, and authorize a credit pull. The lender verifies your income, debts, and credit, then issues a pre-approval letter stating how much you can borrow. With organized documents, most buyers complete this in a few days.

📌 Key Takeaways

- Pre-approval tells you exactly what you can afford before you start touring homes.

- Gathering documents early helps avoid delays and speeds up underwriting.

- A verified pre-approval letter carries real weight with sellers.

- Keep your finances stable before closing to protect your approval.

Introduction

If you are thinking about buying a home, the single most important thing you can do before you look at a single listing is get pre-approved for a mortgage.

Pre-approval tells you exactly how much home you can afford. It tells sellers that you are a serious, qualified buyer. And it gives you the leverage to move quickly in a competitive market — because in California, good homes do not wait around.

The process is simpler than most people think. Here is exactly how it works.

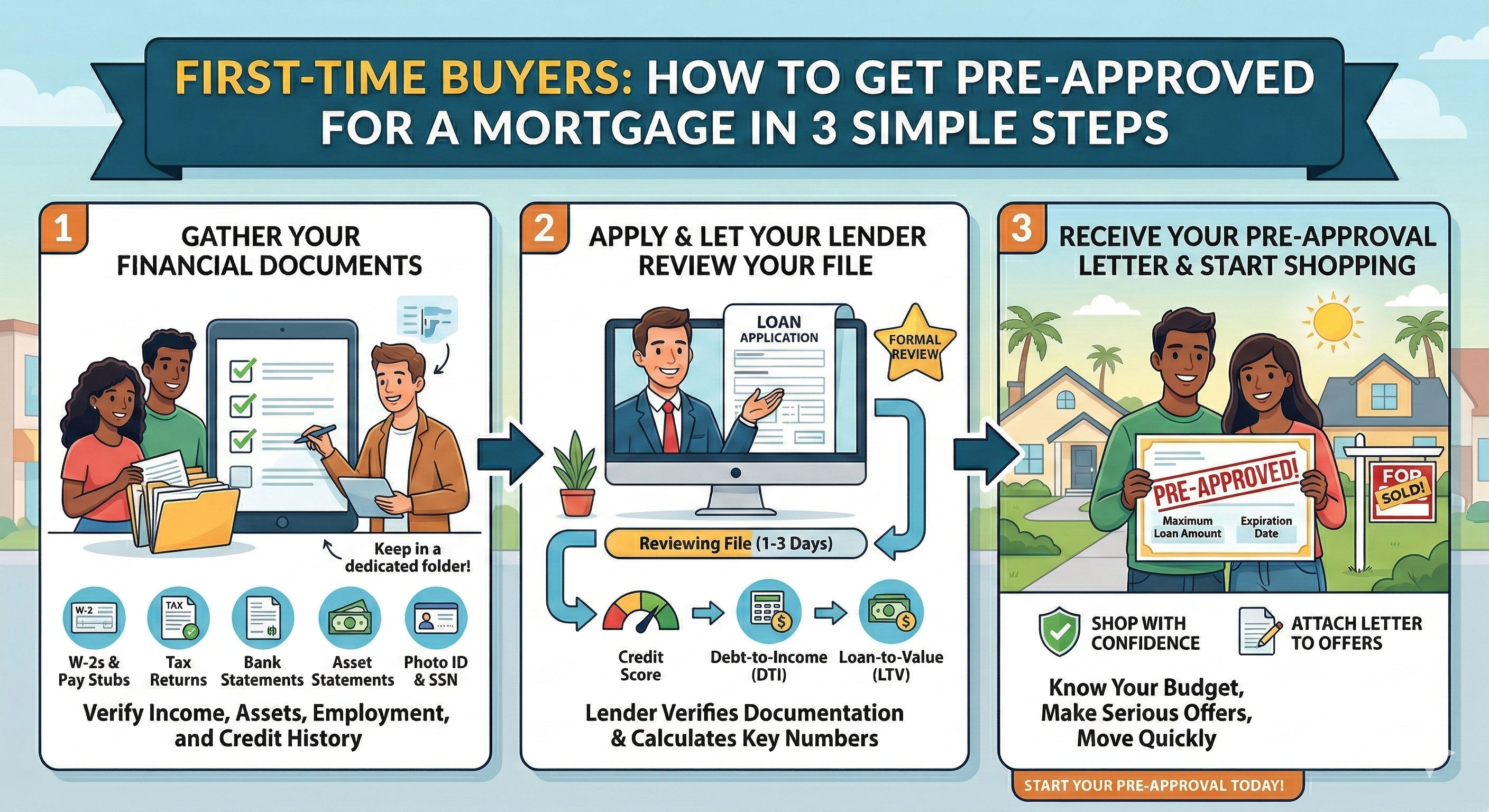

Step 1: Gather Your Financial Documents

Your lender needs to verify your income, assets, employment, and credit history. Gathering these documents before you start the application will make the process significantly faster.

Here is the standard document checklist:

Income Verification

- W-2 employees: Last two years of W-2s and your two most recent pay stubs

- Self-employed: Last two years of personal and business tax returns, plus a year-to-date Profit and Loss statement

- Rental income: Lease agreements and Schedule E from your tax returns

- Other income: Social Security award letters, pension statements, divorce decree (if applicable for alimony/child support)

Asset Documentation

- Two most recent bank statements (all pages) for checking and savings accounts

- Most recent statements for investment accounts, 401(k), IRA, or other retirement accounts

- Gift letter if any portion of your down payment is a gift from a family member

Identity and Credit

- Government-issued photo ID (driver's license or passport)

- Social Security number (your lender will pull your credit report with your authorization)

Pro tip: Have all of these in a folder — physical or digital — before your first conversation with your mortgage advisor. It will save you from the back-and-forth email chase that delays most applications.

Step 2: Apply and Let Your Lender Review Your File

Once your documents are ready, your mortgage advisor will take you through a formal loan application — either in person, over the phone, or online. This is called a Uniform Residential Loan Application (also known as a 1003 form).

Your application will cover:

- Personal information and employment history

- Monthly income and current monthly debt obligations

- The type of loan you are seeking and the estimated home price

- Authorization to pull your credit report

Once your application is submitted, your lender will review your file and issue a pre-approval letter — typically within 1 to 3 business days. Some lenders offer same-day pre-approvals for straightforward files.

During the review, your lender will calculate three important numbers:

- Your credit score: Pulls from all three bureaus (Experian, TransUnion, Equifax) and uses the middle score.

- Your debt-to-income ratio (DTI): Total monthly debt payments divided by gross monthly income. Most loan programs want a DTI of 43% or lower, though some go higher.

- Your loan-to-value ratio (LTV): The loan amount divided by the home's purchase price. Lower LTV (larger down payment) means better terms.

What is the difference between pre-qualification and pre-approval? Pre-qualification is a quick estimate based on self-reported information. Pre-approval is a formal review with verified documentation. Only pre-approval carries weight with sellers.

Step 3: Receive Your Pre-Approval Letter and Start Shopping

Once approved, your lender will issue a pre-approval letter stating the maximum loan amount you qualify for, the loan type, and the expiration date (typically 60-90 days).

Here is how to use your pre-approval effectively:

- Shop below your maximum. Just because you qualify for $650,000 does not mean you should spend $650,000. Think about monthly payment comfort, property taxes, insurance, and maintenance.

- Include the letter with every offer. Your real estate agent will attach your pre-approval letter to every offer you submit. Sellers will not take offers seriously without it.

- Act quickly when you find the right home. Pre-approved buyers who have their documents ready can often get a loan fully processed in 21-30 days — a significant advantage in competitive markets.

- Do not change your financial situation. No new credit accounts, car loans, or major purchases until after closing. Even a small change to your debt or credit score can affect your loan.

What Happens After Pre-Approval?

Pre-approval is the first milestone, not the finish line. Here is what comes next after you have an accepted offer:

- Formal Loan Application: Your pre-approval becomes a full application tied to a specific property.

- Home Appraisal: Your lender orders an appraisal to confirm the home is worth the purchase price.

- Underwriting: An underwriter reviews your full file and the property details for final approval. This is where any remaining conditions are resolved.

- Clear to Close: Once the underwriter approves the file, you receive your Closing Disclosure and schedule your closing date.

- Closing Day: You sign the final documents, funds are transferred, and you get the keys.

From accepted offer to closing typically takes 21-45 days depending on loan type and how quickly conditions are satisfied. A prepared buyer with an organized file is the biggest factor in keeping that timeline tight.

Final Thoughts

Getting pre-approved is not complicated — it is just a matter of gathering your documents, working with the right lender, and taking the first step. The whole process takes a few days and costs nothing.

If you are thinking about buying in California and want to know exactly what you qualify for, I would love to connect. The first conversation is always free, always honest, and always focused on what is best for you.

Ready to get pre-approved? Start today with a free consultation with Rudy Corona. Rudy will review your situation, explain your options, and get you a pre-approval letter you can shop with confidence. Visit the Contact page to get started.

Ready to Get Pre-Approved?

A quick 20-minute call can map your budget, required documents, and next step toward a confident offer strategy.