Quick Answer

If you are a first-time buyer in Southern California, start by getting pre-approved, setting a realistic monthly budget (mortgage plus taxes, insurance, and HOA), and checking down payment assistance before you tour homes. Know local loan limits and competition—South Bay prices and programs differ from the Inland Empire. These four steps prevent the most common mistakes: shopping above your budget, missing assistance, and making weak offers.

📋 What You Will Learn in This Article

- Why pre-approval should happen before touring homes

- What costs to plan for beyond the down payment

- How credit score guidelines vary by loan type

- Which first-time buyer loan options may fit your file

- How to choose a mortgage advisor who protects your interests

Introduction

Buying your first home in Southern California is one of the most exciting — and honestly, one of the most overwhelming — financial decisions you will ever make. Between rising home prices, competitive bidding wars, and mortgage jargon that sounds like a foreign language, it is easy to feel lost before you have even looked at a single listing.

I am Rudy Corona, a licensed Mortgage Advisor serving homebuyers all across Southern California. Over the years, I have helped hundreds of first-time buyers navigate this process — and I have seen the same five mistakes and misconceptions come up again and again. This guide is my way of making sure you do not have to learn them the hard way.

Let us get into it.

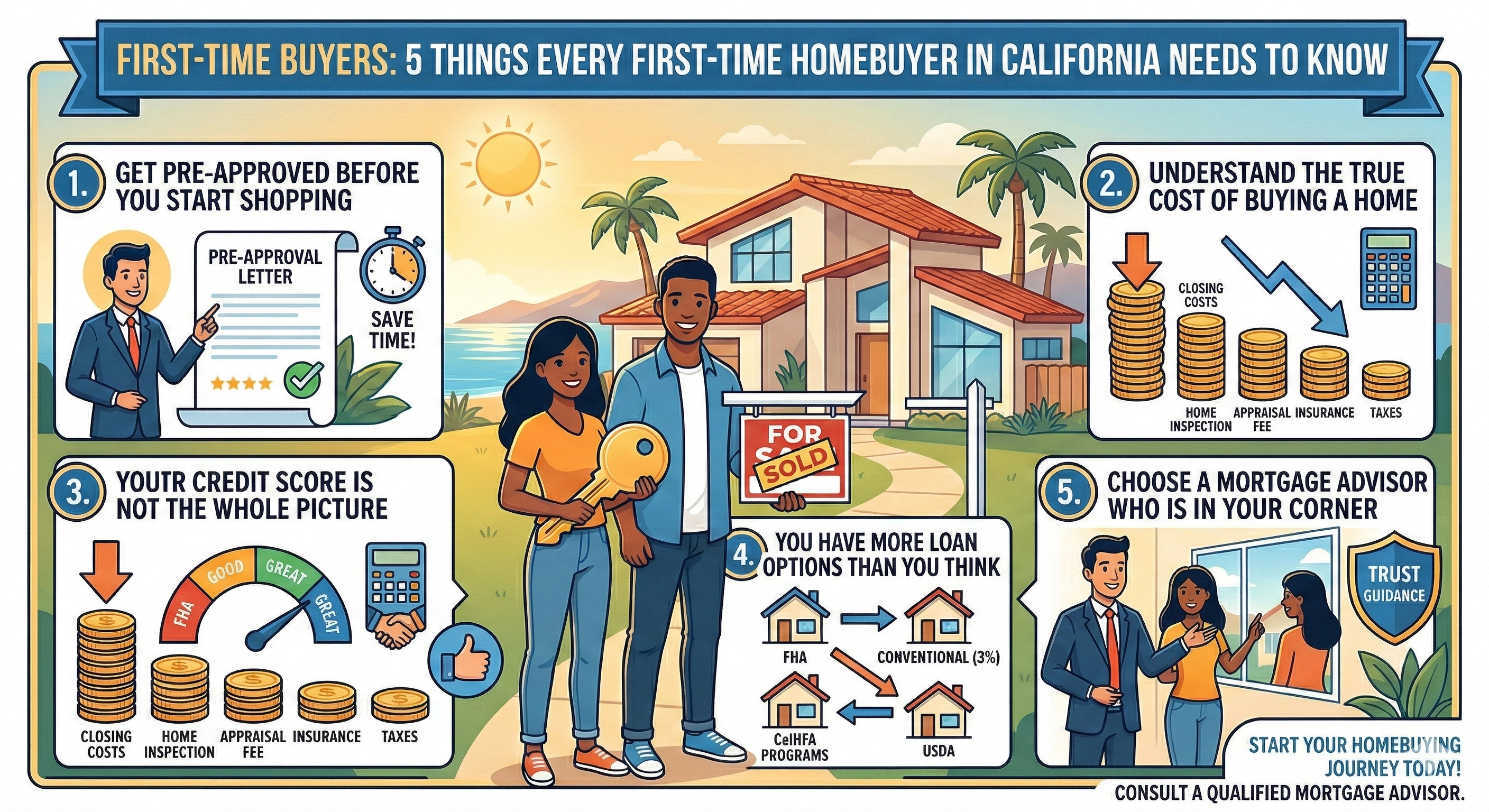

1. Get Pre-Approved Before You Start Shopping

This is the single most important step most first-time buyers skip. They find a home they love, fall in love with it, and then scramble to figure out financing — only to lose it to a buyer who was already pre-approved.

Pre-approval is not the same as pre-qualification. Pre-qualification is a quick estimate based on what you tell a lender. Pre-approval is a formal review of your credit, income, assets, and debt — and it gives you a real number to shop with.

In Southern California's competitive market, sellers will not take you seriously without a pre-approval letter. The good news: the pre-approval process is free, it takes only a few days, and it puts you in a strong position to move fast when the right home comes along.

Pro Tip: Get pre-approved with a local mortgage advisor, not just an online lender. Local advisors know the SoCal market, have relationships with listing agents, and can often help you close faster.

2. Understand the True Cost of Buying a Home

The down payment gets all the attention, but it is not the only cost you need to plan for. First-time buyers are often surprised by the full picture of what they need at closing — and beyond.

Here is what you should budget for in addition to your down payment:

- Closing costs: Typically 2-5% of the loan amount. On a $500,000 home, that is $10,000-$25,000.

- Home inspection: $400-$700, paid out of pocket before closing.

- Appraisal fee: Usually $500-$800, required by your lender.

- Homeowners insurance: First year is often paid at closing.

- Property taxes: Depending on timing, you may owe a partial year at closing.

- Moving costs and immediate repairs: Budget at least a small cushion for surprises.

The good news is that programs exist to help first-time buyers with down payment and closing cost assistance. Ask me about what is available in your area — you may qualify for more help than you think.

3. Your Credit Score Is Not the Whole Picture

Many first-time buyers assume their credit score needs to be perfect to buy a home. That is simply not true. Different loan programs have different requirements, and a good mortgage advisor will help you find the best option for your situation.

Here is a quick breakdown:

- Conventional Loans: Generally require a 620+ credit score.

- FHA Loans: Allow scores as low as 580 with a 3.5% down payment, or even 500 with 10% down.

- VA Loans: No official minimum score for eligible veterans — lenders vary.

- Down payment assistance programs: Often have their own credit requirements, usually 620+.

Even if your credit needs work, do not give up. A good mortgage advisor will help you understand exactly where you stand and what steps — if any — you should take to improve your position before applying.

Important: Do NOT open new credit cards, finance a car, or make any large purchases between pre-approval and closing. This can change your debt-to-income ratio and jeopardize your loan.

4. You Have More Loan Options Than You Think

Most first-time buyers have heard of a 30-year fixed mortgage and not much else. But the reality is there are several loan types worth understanding, each with different requirements and benefits.

The most common options for first-time buyers in California include:

- FHA Loans: Lower credit score requirements and down payments as low as 3.5%. Great for buyers with limited savings or less-than-perfect credit.

- Conventional Loans (3% down): If your credit is solid, you can put as little as 3% down on a conventional loan without the upfront mortgage insurance premium that FHA requires.

- CalHFA Programs: California Housing Finance Agency offers down payment assistance programs specifically for first-time California buyers. These can cover part of your down payment or closing costs.

- USDA Loans: If you are purchasing in a rural or suburban area, USDA loans offer zero-down financing with competitive rates.

The right loan depends on your credit, income, savings, and goals. That is exactly why a conversation with a local mortgage advisor is worth more than hours of online research.

5. Choose a Mortgage Advisor Who Is in Your Corner

Not all lenders are equal. Big banks have rigid underwriting and limited flexibility. Online lenders can leave you without answers when questions come up. And some brokers care more about their commission than your best outcome.

What you want is a mortgage advisor who acts like a guide — someone who takes the time to understand your situation, explains your options in plain English, shops multiple lenders on your behalf, and stays by your side from application to closing day.

Ask your mortgage advisor these questions before you commit:

- How long does your typical process take from pre-approval to closing?

- Do you have access to multiple lenders, or are you limited to one?

- Are there any loan programs for first-time buyers you think I should consider?

- How will you communicate with me throughout the process?

Your home is the biggest purchase of your life. Make sure the person helping you finance it is someone you can trust.

Final Thoughts

Buying your first home in Southern California is absolutely achievable — even in today's market. The key is going in educated, prepared, and with the right team in your corner.

If you have questions about any of this, or if you want to find out exactly what you qualify for, I would love to have a conversation. The first consultation is always free.

Ready to take the first step? Book your free mortgage consultation with Rudy Corona. No pressure, no commitment — just answers. Visit the Contact page to get started.

Buying Your First Home in SoCal? Start With a Plan

Get pre-approved, understand your costs, and shop with confidence in a free 20-minute consultation.